[Leaving same post date, but a quick update here March 27: It took two weeks, but my headlined forecast proved true as of the week ending March 23 — as shown by an AP story out of Pittsburgh reporting PA was now down to hosting 98 active rigs.]

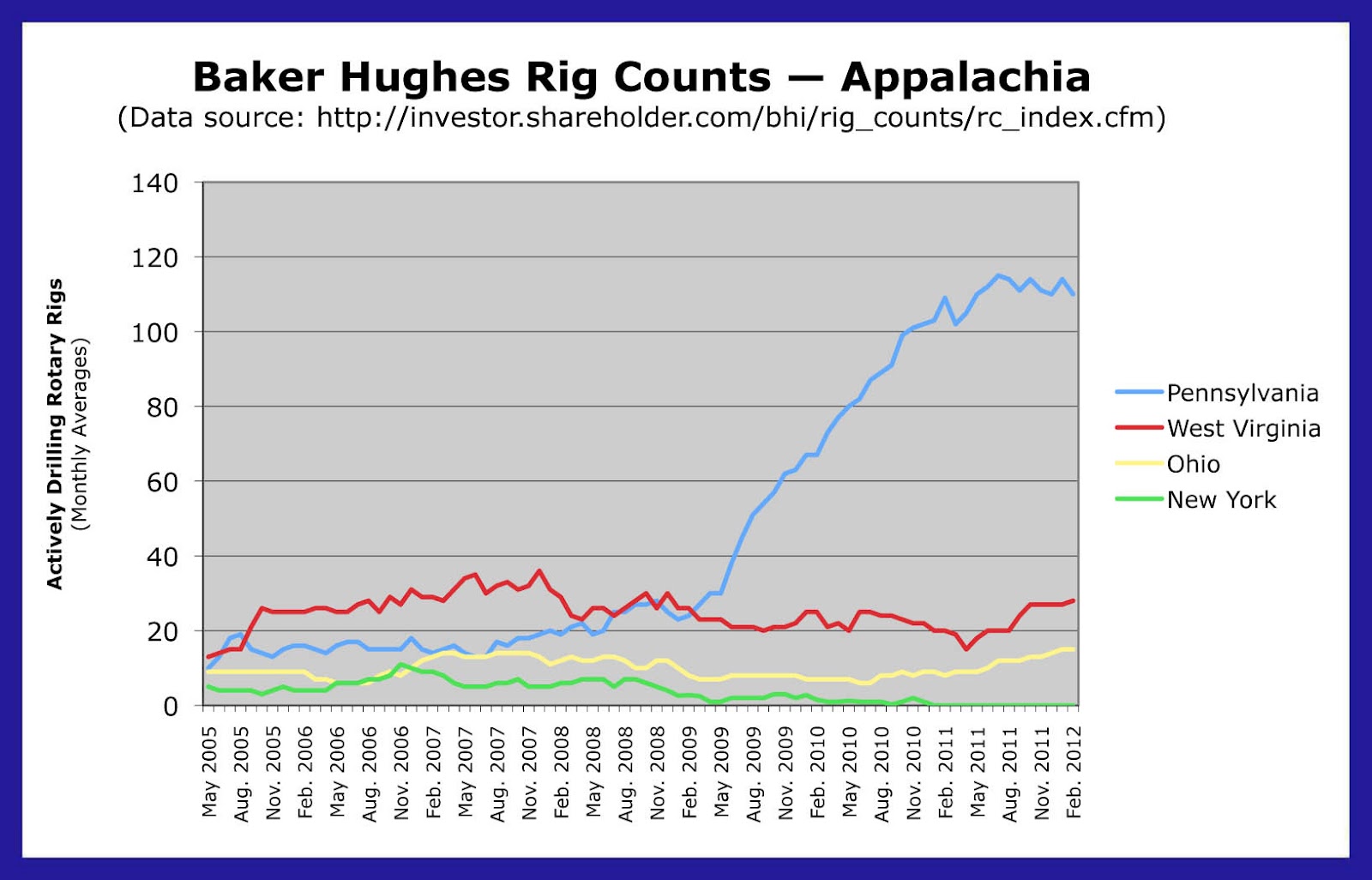

It doesn't show on my chart yet, because that's based on monthly averages, and the month of March is still going on. But the weekly active rig numbers issued by oil patch service behemoth Baker Hughes today, March 9, (and at Noon Central Time every Friday), show Pennsylvania having "only" 101 such operations at work in-state.

That's a drop of nine compared to the February 2012 monthly average, and a drop of four from just the prior week. It's a pretty good sign the Keystone State will soon be dropping below the nice round threshold of 100 rigs. The last time PA hosted fewer than 100 actually drilling rigs was in Oct. 2010, during a time period when it was on a run-up to its record high of 115 rigs, reached in July 2011.

Meanwhile, based on the last full monthly averages, Ohio had 15 rigs at work, and West Virginia had 28 — both states appearing to continue slight upward trends over the last ten months or so. New York, needless to say, scored another 0. In fact, the last time NY had a rig working in-state big enough for Baker Hughes to find it was back in December 2010.

Since most rigs are working on a single well during any given week, the ebb and flow of employment impact can be roughly correlated to the rig counts using the figure of approximately 420 jobs per well — based on the assumptions used in a July 2011 study by an arm of Penn State Extension. While most Easterners can envision only pickup-driving roughnecks from out of state, jobs tied to fossil fuels extraction are actually spread across more than 150 different occupations — each hard at work in their respective fields, before, during, and after drilling.

A drilling boom in Ohio has been anticipated for months in connection with Summer 2011 revelations that eastern parts of the Buckeye State are blessed with shale gas, shale gas liquids, and shale oil — all from the previously under-recognized rock layer known as Utica shale. The wetter and oilier portions of Ohio's Utica are said to preserve the economics of unconventional prospects due to higher values for these resources compared to pure dry methane. Western PA is also known to host similar "wet" fossil fuels — in the Marcellus, and in the not yet widely discussed Upper Devonian — and that may be part of what's keeping that state's rig count from completely crashing.

Methane's market value, meanwhile, has been repeatedly setting new ten-year lows in the mid-$2-per-MMBTU range for most of the winter of 2011-2012. Those kinds of prices — about one-half or one-third of modern averages — have meant terrific savings for End Consumers, but they are unquestionably alarming for industry, investors, and landowners. The natgas price drop, though previously attributed at least in part to recessional forces, is now much more clearly seen as a supply-demand trough caused largely by the Shale Energy Technological Revolution's remarkably quick creation of a huge glut. With those commodity values, it's equally remarkable there are this many rigs still active at all in Appalachia, where — measured in BTU's, at least — the majority of the undeveloped resource remains in the form of dry natgas.

Moves by industry into northeastern U.S. fields, from 2008 onward, have had the unforeseen political consequence of much more widely publicizing (and making controversial) the previously obscure revolution triggered by hydraulic fracturing — which is now much more commonly (and disparagingly) referenced as "fracking," or "hydrofracking." Contrary to virtually all shorthand descriptions appearing in northeastern media, hydraulic fracturing is not so much a drilling technique, as it is a "completion" technique — most profitably deployed within deep horizontal wellbores drilled beforehand for that purpose. It is an American technological feat which combines the 1940s-invented fracking, accomplished vertically, with the also 1940s-invented horizontal drilling, and it was pioneered by independent operators (with some federal R&D help, as President Obama recently noted) in the Barnett Shale of Texas.

Though widely and misleadingly described by overdramatic northeastern media as working by "blasting," "shattering," or "breaking up" the shale — or by "flushing out" the fossil fuels — fracking in actual fact works by simply countering natural rock pressure, temporarily, in discrete, one-at-a-time sections of previously drilled sedimentary bedrock. That high pressure is applied for the purpose of slipping sand (or ceramic beads) into the shalebed's numerous tiny fractures — some old, and some newly created. After the hydraulic pressure is intentionally eased up, and some of the spent frack water recovered, the "proppants" are left behind, stuck in the cracks, keeping routes through the shale open for the fossil fuels to escape to the wellbore, usually under normal rock pressure.

[Some further miscomprehensions peculiar to the East Coast: Fracking has become inextricably linked in the public's mind with natural gas production, but — in actual reality, looking at the full picture in North America or worldwide — the technique is just as important for producing unconventional oil or liquids as natgas. (See, for instance, this recent piece of Reality Correction from the very worthwhile blog of former PA DEP Chief John Hanger.) Furthermore, though you sure don't hear about this much, fracking is also a key part of the arsenal for several much-less-besmirched enterprises, such as geothermal development, drilling more productive water wells, and still-under-development green dreams to work against global warming by sequestering carbon deep underground.]

My chart above runs the rig data back to October 2004, the month when Range Resources quietly became the first driller in the Appalachian basin to stimulate a horizontal Marcellus well in this way. Word of Range's surprisingly successful gas-finding results on this and follow-up wells did not get out widely until January 2008, when geologists Terry Engelder of Penn State and Gary Lash of SUNY Fredonia saw through the arcana of industry reports to investors in order to conclude, and publicly release, a significant upward re-estimation of the natural gas content of the Marcellus formation.

Over the time frame of this technological upheaval, the Baker Hughes rig counts are useful in offering a historical comparison of industry's boom or bust response to the varying economic times, geologic fortunes, and regulatory receptions posed by each of these four states. As you can readily see, drilling in PA was running even or higher nearly every successive month from January 2009 to July 2011, before finally topping out under the downward economic pressure created by the breakthrough's own continent-wide success. While neither OH or WV has (yet) witnessed anything like the drilling boom which took off in PA, both states have stayed open to such developments — being guided by state administrations and political climates favoring the enterprise. In NY, by contrast, industry's interest in developing Upstate landowners' previously unknown shale gas resource has been greeted with a chronically delayed regulatory holdup, meshing obstructively with a gathering political firestorm.

In fact, New York on Feb. 15, 2012 — without any media notice whatsoever — reached the Four-Year Mark for its infamous shale gas moratorium. That is the historical fact if you consider the moratorium's starting point to be Feb. 15, 2008, as I do. That's the date industry first (unsuccessfully) asked for a drilling permit for a full-scale Marcellus well in the state. Five months later, on July 23, 2008, New York officials followed their informal bureaucratic hesitation with a more formalized administrative freeze, pending study of the environmental impacts of high-volume completions, and the crafting of tougher operational rules, a process which is still ongoing.

Over all this time, drilling opponents and sympathetic media representatives have largely succeeded in subtly re-framing New York's ban as being a question of whether or not the state will ever allow shale gas development. Drilling proponents, on the other hand, have insisted upon continuing to view the moratorium as it was originally described — as a temporary measure — preferring to believe that developing the Empire State's indigenous shale gas has always been a matter of when, and how, but not if. Officialdom has cagily gone back and forth, using either characterization, depending on the person, the timing, or the situation — such as this recent, seemingly supportive-of-drilling statement from Governor Andrew Cuomo.

Baker Hughes has long kept a tally of active drilling rigs for both informational and promotional purposes. The counts trace their history to 1944, when they were initiated by predecessor Hughes Tool Company (whose founder Howard Hughes, Sr. invented the two-cone rotary drill bit). The Hughes company realized that its sales force generally knew (or could find out) the location by state or province of every single operating rotary rig in the United States or Canada — even those which weren't (yet) using Hughes tools.

The counts have been consistently maintained ever since, and they have become a barometer for the energy sector, and for the economy generally.

Baker Hughes' rig counts are considered more conservative than those broadcast by other outlets, because they only count active, rotary rigs — highly complex operations which are in the midst of placing substantial economic demands on the service, support, and labor sectors.

Rigs are only counted as active if they are being employed anywhere along the line between "spudding in" (or starting a well) and "target depth." Not counted are rigs that are in the process of being taken down, moved, or rigged up again, or rigs that are being used to support non-drilling chores, such as workovers, completions, or testing. Most relatively small, cable-tool and truck-mounted setups are also excluded from the census.

It doesn't show on my chart yet, because that's based on monthly averages, and the month of March is still going on. But the weekly active rig numbers issued by oil patch service behemoth Baker Hughes today, March 9, (and at Noon Central Time every Friday), show Pennsylvania having "only" 101 such operations at work in-state.

That's a drop of nine compared to the February 2012 monthly average, and a drop of four from just the prior week. It's a pretty good sign the Keystone State will soon be dropping below the nice round threshold of 100 rigs. The last time PA hosted fewer than 100 actually drilling rigs was in Oct. 2010, during a time period when it was on a run-up to its record high of 115 rigs, reached in July 2011.

Meanwhile, based on the last full monthly averages, Ohio had 15 rigs at work, and West Virginia had 28 — both states appearing to continue slight upward trends over the last ten months or so. New York, needless to say, scored another 0. In fact, the last time NY had a rig working in-state big enough for Baker Hughes to find it was back in December 2010.

Since most rigs are working on a single well during any given week, the ebb and flow of employment impact can be roughly correlated to the rig counts using the figure of approximately 420 jobs per well — based on the assumptions used in a July 2011 study by an arm of Penn State Extension. While most Easterners can envision only pickup-driving roughnecks from out of state, jobs tied to fossil fuels extraction are actually spread across more than 150 different occupations — each hard at work in their respective fields, before, during, and after drilling.

A drilling boom in Ohio has been anticipated for months in connection with Summer 2011 revelations that eastern parts of the Buckeye State are blessed with shale gas, shale gas liquids, and shale oil — all from the previously under-recognized rock layer known as Utica shale. The wetter and oilier portions of Ohio's Utica are said to preserve the economics of unconventional prospects due to higher values for these resources compared to pure dry methane. Western PA is also known to host similar "wet" fossil fuels — in the Marcellus, and in the not yet widely discussed Upper Devonian — and that may be part of what's keeping that state's rig count from completely crashing.

Methane's market value, meanwhile, has been repeatedly setting new ten-year lows in the mid-$2-per-MMBTU range for most of the winter of 2011-2012. Those kinds of prices — about one-half or one-third of modern averages — have meant terrific savings for End Consumers, but they are unquestionably alarming for industry, investors, and landowners. The natgas price drop, though previously attributed at least in part to recessional forces, is now much more clearly seen as a supply-demand trough caused largely by the Shale Energy Technological Revolution's remarkably quick creation of a huge glut. With those commodity values, it's equally remarkable there are this many rigs still active at all in Appalachia, where — measured in BTU's, at least — the majority of the undeveloped resource remains in the form of dry natgas.

Moves by industry into northeastern U.S. fields, from 2008 onward, have had the unforeseen political consequence of much more widely publicizing (and making controversial) the previously obscure revolution triggered by hydraulic fracturing — which is now much more commonly (and disparagingly) referenced as "fracking," or "hydrofracking." Contrary to virtually all shorthand descriptions appearing in northeastern media, hydraulic fracturing is not so much a drilling technique, as it is a "completion" technique — most profitably deployed within deep horizontal wellbores drilled beforehand for that purpose. It is an American technological feat which combines the 1940s-invented fracking, accomplished vertically, with the also 1940s-invented horizontal drilling, and it was pioneered by independent operators (with some federal R&D help, as President Obama recently noted) in the Barnett Shale of Texas.

Though widely and misleadingly described by overdramatic northeastern media as working by "blasting," "shattering," or "breaking up" the shale — or by "flushing out" the fossil fuels — fracking in actual fact works by simply countering natural rock pressure, temporarily, in discrete, one-at-a-time sections of previously drilled sedimentary bedrock. That high pressure is applied for the purpose of slipping sand (or ceramic beads) into the shalebed's numerous tiny fractures — some old, and some newly created. After the hydraulic pressure is intentionally eased up, and some of the spent frack water recovered, the "proppants" are left behind, stuck in the cracks, keeping routes through the shale open for the fossil fuels to escape to the wellbore, usually under normal rock pressure.

[Some further miscomprehensions peculiar to the East Coast: Fracking has become inextricably linked in the public's mind with natural gas production, but — in actual reality, looking at the full picture in North America or worldwide — the technique is just as important for producing unconventional oil or liquids as natgas. (See, for instance, this recent piece of Reality Correction from the very worthwhile blog of former PA DEP Chief John Hanger.) Furthermore, though you sure don't hear about this much, fracking is also a key part of the arsenal for several much-less-besmirched enterprises, such as geothermal development, drilling more productive water wells, and still-under-development green dreams to work against global warming by sequestering carbon deep underground.]

My chart above runs the rig data back to October 2004, the month when Range Resources quietly became the first driller in the Appalachian basin to stimulate a horizontal Marcellus well in this way. Word of Range's surprisingly successful gas-finding results on this and follow-up wells did not get out widely until January 2008, when geologists Terry Engelder of Penn State and Gary Lash of SUNY Fredonia saw through the arcana of industry reports to investors in order to conclude, and publicly release, a significant upward re-estimation of the natural gas content of the Marcellus formation.

Over the time frame of this technological upheaval, the Baker Hughes rig counts are useful in offering a historical comparison of industry's boom or bust response to the varying economic times, geologic fortunes, and regulatory receptions posed by each of these four states. As you can readily see, drilling in PA was running even or higher nearly every successive month from January 2009 to July 2011, before finally topping out under the downward economic pressure created by the breakthrough's own continent-wide success. While neither OH or WV has (yet) witnessed anything like the drilling boom which took off in PA, both states have stayed open to such developments — being guided by state administrations and political climates favoring the enterprise. In NY, by contrast, industry's interest in developing Upstate landowners' previously unknown shale gas resource has been greeted with a chronically delayed regulatory holdup, meshing obstructively with a gathering political firestorm.

In fact, New York on Feb. 15, 2012 — without any media notice whatsoever — reached the Four-Year Mark for its infamous shale gas moratorium. That is the historical fact if you consider the moratorium's starting point to be Feb. 15, 2008, as I do. That's the date industry first (unsuccessfully) asked for a drilling permit for a full-scale Marcellus well in the state. Five months later, on July 23, 2008, New York officials followed their informal bureaucratic hesitation with a more formalized administrative freeze, pending study of the environmental impacts of high-volume completions, and the crafting of tougher operational rules, a process which is still ongoing.

Over all this time, drilling opponents and sympathetic media representatives have largely succeeded in subtly re-framing New York's ban as being a question of whether or not the state will ever allow shale gas development. Drilling proponents, on the other hand, have insisted upon continuing to view the moratorium as it was originally described — as a temporary measure — preferring to believe that developing the Empire State's indigenous shale gas has always been a matter of when, and how, but not if. Officialdom has cagily gone back and forth, using either characterization, depending on the person, the timing, or the situation — such as this recent, seemingly supportive-of-drilling statement from Governor Andrew Cuomo.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Baker Hughes has long kept a tally of active drilling rigs for both informational and promotional purposes. The counts trace their history to 1944, when they were initiated by predecessor Hughes Tool Company (whose founder Howard Hughes, Sr. invented the two-cone rotary drill bit). The Hughes company realized that its sales force generally knew (or could find out) the location by state or province of every single operating rotary rig in the United States or Canada — even those which weren't (yet) using Hughes tools.

The counts have been consistently maintained ever since, and they have become a barometer for the energy sector, and for the economy generally.

Baker Hughes' rig counts are considered more conservative than those broadcast by other outlets, because they only count active, rotary rigs — highly complex operations which are in the midst of placing substantial economic demands on the service, support, and labor sectors.

Rigs are only counted as active if they are being employed anywhere along the line between "spudding in" (or starting a well) and "target depth." Not counted are rigs that are in the process of being taken down, moved, or rigged up again, or rigs that are being used to support non-drilling chores, such as workovers, completions, or testing. Most relatively small, cable-tool and truck-mounted setups are also excluded from the census.

2 comments:

You are a bit early with your fourth anniversary celebration. The bill that set spacing units for horizontal shale wells was not passed until 23 June. It wasn't practical to drill until those spacings became law.

That's a good point -- though I wonder if DEC had the power to give spacing variances under the prior version of the law. It definitely would have been more cumbersome to do it that way for every shale gas application, which is the main reason why they amended the law in 2008.

Post a Comment