|

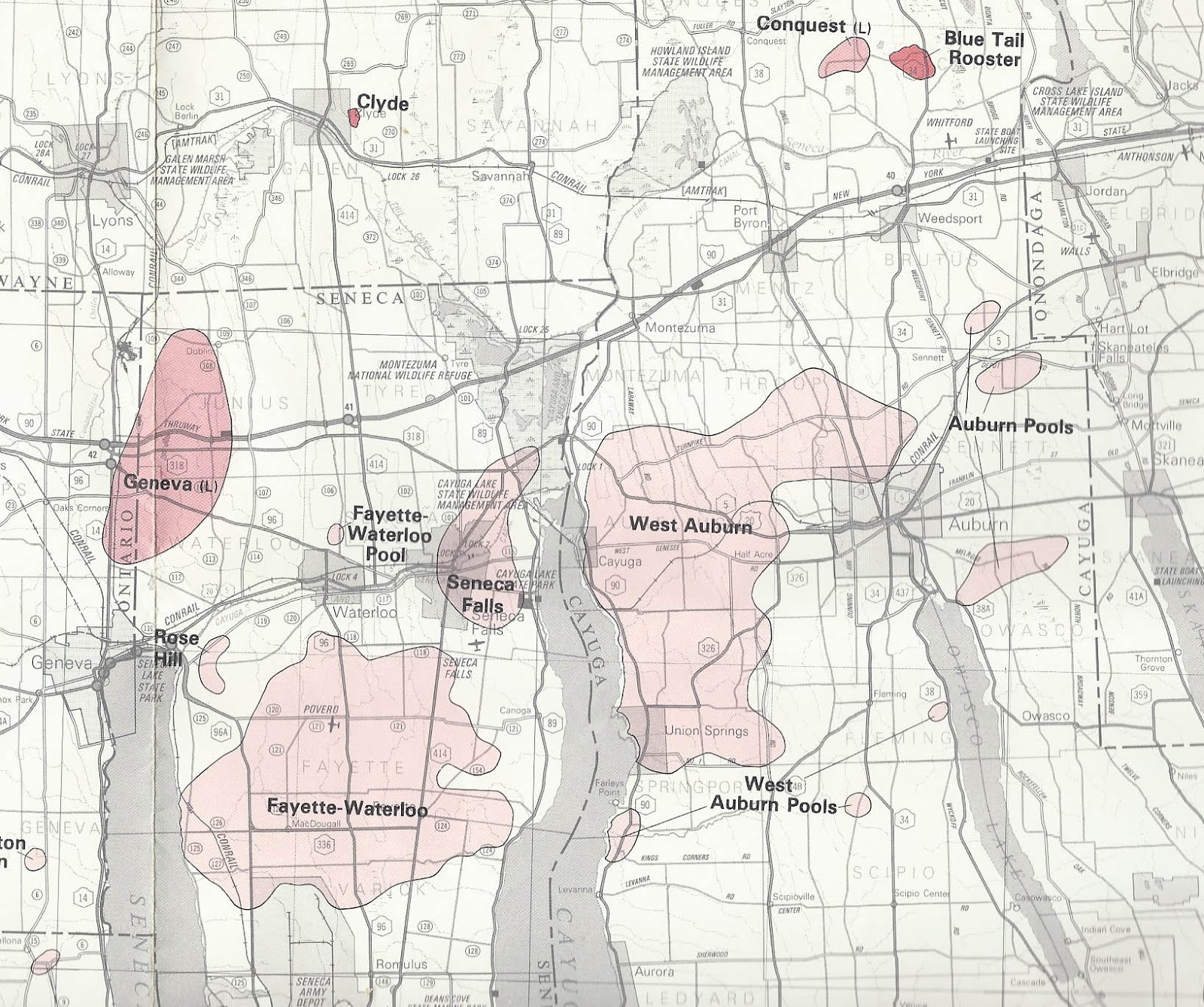

| Location and sprawl of the Fayette-Waterloo and West Auburn natural gas fields, as approximated by the NYS DEC on a really nice wall map put out back in 1986. Producing gas wells here appear to be the primary asset recently transferred between Chesapeake and Minard Run. |

[Original post March 19, 2012. Updated March 20 to account for some curve balls which I either missed the first time through, or were later thrown into the electronic records.]

Some unreported oil and gas news became available late last week for those few Upstaters who were not outdoors sunning themselves, but instead were locked indoors, combing the NYS DEC's oil and gas databases, which cover well permits, transfers, and production.

Here it is: Chesapeake Energy — the nation's number two natural gas producer, based in Oklahoma, and prior absorber of leading Appalachian producer Columbia Natural Resources — recently sold 415 natural gas wells to Minard Run Oil Co. of the City of Bradford, Pennsylvania. Minard Run traces its origins back to 1875 in the western PA epicenter of the world's original oil boom, and has long boasted it is the world's oldest family-owned independent — in fact continuously owned by the same family.

The transfer requests were submitted March 14, and approved by the DEC March 15. The computer records were updated soon thereafter. The state has a bureaucratic role in keeping tabs on these otherwise completely private transactions because it enforces the public interest in maintaining a responsible party for each well (and — little-appreciated fact here — in making sure local assessors get the gas well tax bills mailed to the right payer).

I have seen no announcement on this yet from either CHK or Minard Run. But, barring some kind of major malfunction in the electronic records, that's the story, as revealed by a close reading of this otherwise arcane data.

On the basis of well counts, if not actual production, the selection of assets represents most of CHK's New York portfolio of active (or potentially active) wellheads — all, that is, except for its high-producing, horizontally or directionally drilled Trenton-Black River limestone efforts. As of the time of this writing, CHK is still the listed operator of 64 active, (or potentially active) wells, mostly TBR's, and mostly in the mid-southern or mid-central parts of the state.

Most of the recently transferred wells are in Queenston sandstone production zones ranging across the mid-sections of two Finger Lakes counties — Cayuga (211 wells, all Queenston), and Seneca (184, all Queenston except for two verticals in obscure shales). These traditional, vertically developed fields have been producing natural gas with little public notice or controversy since they originally broke out in the 1960s. Known to New York's handful of gas patch veterans as the West Auburn and Fayette-Waterloo fields, CNR bought these interests in 1999. In 2005, CHK made its entry into Appalachia by buying up CNR basin-wide.

Included on the CHK-to-Minard-Run list are a number of other generally not-yet-producing wells sparsely populating six surrounding counties: Wayne (2 TBR wells); Ontario (1 Queenston); Yates (5 total — 3 Queenston's and 2 not applicable's); Schuyler (3 Queenston's); Cortland (1 not applicable); and Onondaga (8 Queenston's).

Some of these additional wells were initiated as TBR efforts, but — having proved dry at that horizon — were plugged back to shallower zones more capable of production, as discovered on the way down, either by design or happenstance. Predecessor CNR was the originator of the TBR play in New York (in Steuben County — where the discovery well was drilled as early as 1985, the field further developed in 1995, and word got out circa 1998). Since 2008, however, these sorts of historically uncontroversial exploration efforts have been popularly forgotten in the tussle over hydraulic fracturing for shale gas, which is still not permitted on a full scale horizontal basis in New York.

Like shale, TBR represents a high-tech campaign, but, as contrasted to shale, it requires much more involved seismic study in advance of pinpoint drilling, and a gambler's willingness to run the risk of a dry hole (which turned out to be substantial). Other operators followed CNR's breakthroughs in seismic interpretation with even better results, as represented by the suite of TBR mega-producers in Chemung, Schuyler, and Steuben counties, most of which were either developed, or purchased after development, by the Canadian operator Talisman Energy, f/k/a Fortuna. Partly due to a shift in investment interest toward fully permitable shale gas out of state, and partly due to sinking market values for natural gas, no new TBR efforts have been drilled in New York since August 2010, when Anschutz Exploration spudded the Dow 2 in Chemung County.

Queenston development has been similarly weak in recent years: Only three wells listing that rock layer as the intitial target have been started since 2009.

New York's unfortunate state of drilling decline has been covered by this blog in much greater detail here.

CHK had been rumored for at least a couple years to be willing to entertain a buyer for its relatively low-volume, old-school producers. This move now in New York appears to connect with the company's announced sales of other assets nationally — which have been publicly explained as a way of raising operating cash and driving down debt, both of which have long been lodged as concerns by investors and stock analysts.

I do not know yet to what extent the deal includes CHK's thousands of acres in undeveloped leases. These are in part geographically intermingled with these wells — which, by definition, drain areas covered by developed, indefinitely running, held-by-production leases (and which therefore would logically have to pass with well ownership, including at least rights to the productive zones). Some of CHK's undeveloped leases are still ticking within their generally five- or ten-year primary terms, and some may be subject to extensions on grounds of force majeure — due to the superior, unforeseen, disruptive force caused by New York State's now Four-Year-Old Regulatory Sink Hole on Shale Gas. It remains to be seen whether NY courts will view the state's shale gas blockade as enough of a reason for leaseholders to legitimately invoke this Contracts Law 101 clause. There are at least a couple cases underway, brought by landowners who are primarily motivated by the hope of being someday free to lease again for more money, higher royalty, and more protectively drafted terms — now that the shale gas genie is out of the bottle.

Note, however, that the locations of the CHK-to-Minard-Run wells are generally too far north or west within Upstate to have obvious, near-term relevance for shale gas. That's if you believe, as several geologists have put forth, the Marcellus shale is too shallow or too thin in these areas, and the Utica shale remains too much of an unknown. I say this despite substantial "They're gonna drill everywhere!" hype broadcast hereabouts over the last four years as part of the Ongoing Shale Gas Showdown. As I've written before, some of that persuasive misdirection has come from the excessively hopeful pro-drilling side, while another five or six helpings' worth have come from the excessively fearful, kill-the-drill side — acting in rare, unscripted agreement with their debating partners.

That being the case, this latest transaction may not represent CHK's loss of interest, or loss of confidence, in some day fracking for shale gas in New York — should the Cuomo Administration finally find a way to push through some Regulatory Resolve on this question. CHK could still develop natural gas from the Marcellus under current or future leases closer to the heart of the play in the Southern Tier, hugging the State Line, where the shale is virtually a slam dunk, based on production data from PA.

In addition to the number of acres involved, the other main question is the sale price for the overall transaction, which will have to await formal announcements from the buyer or seller. It may wind up being too minor of a transaction — in the context of CHK's much more involved balance sheet — to be detailed in future quarterly reports.

No comments:

Post a Comment